Understanding our 6 C’s of Business Lending

efund

March 1, 2023

Entrepreneur Fund Credit Manager Zack Hoy, right, meets with Anna and Nathanael Bailey, owners of Bailey Builds in Duluth, Minnesota.

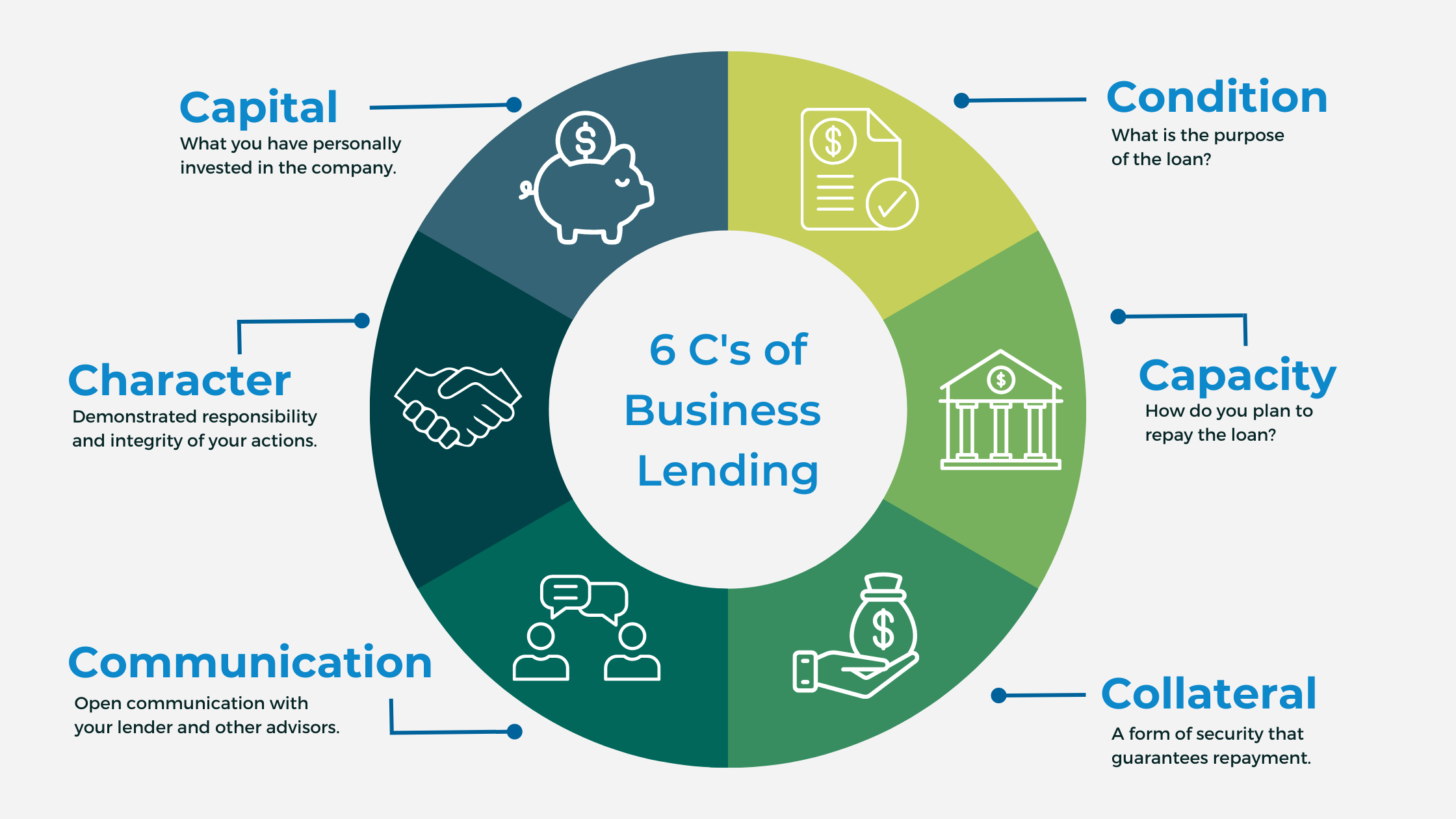

Whether you’re seeking a business loan to purchase new equipment, build a cash reserve for your seasonal business, renovate your shop, or expand your business in some way, there are five areas that are universally considered by lenders before granting a loan: character, capacity, capital, collateral, and conditions. At EFund we add a sixth C to the process that we believe is key to financial partnership – communication.

Learn what our lending team looks for when they work with small businesses. Understanding these criteria can help your chances and increase the efficiency in which your loan is approved.

So, let’s dive a little deeper into our 6 C’s of Business Lending:

1. Character

When we think about character, we think about the attributes needed to run a business:

- Have you owned a business?

- Do you have experience in this type of business?

- Are you eager to learn and are you coachable?

- Do you have a business mentor or professionals you rely on?

Character also looks at your past performance with credit that you’ve been granted. Do you pay your bills on time? A poor credit score is not an automatic out for the Entrepreneur Fund, but it does require a written explanation.

You can help your chances for approval by:

- Writing a resume tailored to your business idea.

- Resolving any significant credit issues prior to applying.

- Checking your credit report for free at www.annualcreditreport.com

2. Capacity

Have your paperwork ready for your loan officer because this is how you prove your ability to repay the loan:

- tax returns

- profit & loss report

- balance sheet

- debt schedule

- cash flow projections

Your loan officer will review your financial statements. Their job is to validate your loan request by demonstrating your companies’ ability to pay all of its bills and to pay you. Having accurate financial information makes the capacity decision easier. Projections and assumptions explain what you believe will happen and will offer confidence to your lender.

You can help your chances for approval by:

- Offering explanations about large one-time expenses that make your financials look poor.

- Spending time building a great cash flow projection. Details matter! Write an assumptions page to explain how you came up with your revenues and expenses in your cash flow projection.

- Reaching out to your Entrepreneur Fund business advisor. They’re able to help with these processes.

- Review these financial tools to help you better prepare your paperwork.

3. Capital

Investing some of your own money in a project is a must for loan approval. Banks typically request between 10% to 30% of your own money at risk in a project before they will commit. At EFund, we request around 10%.

There are strategies to help you if the bank needs you to come in with more than you have. Some ideas include:

- the seller holds a note for a portion of the deal

- securing gap financing from EFund (around 30% of our loans are gap financing deals with our banking partners)

- you receive a financial gift from a relative or friend

Do you have a plan B? What if your project is 90% completed and your contractor finds a costly unexpected issue. How can you finish the project? Will your bank help you with additional funds?

You can help your chances for approval by:

- Planning ahead for your down payment requirement.

- Talking with gap lenders, like EFund, about additional financing.

- Build additional personal savings to allow for emergencies.

4. Collateral

Remember that except for credit cards, most loans require collateral. Business loans are no different. What is collateral? Collateral is something pledged as security for repayment of a loan, to be forfeited in the event of a default. If you are not willing to pledge collateral, it is very difficult for your loan officer to get an approval of your loan request.

All collateral is not equal. Real estate holds a strong collateral value of 80% to 90%, whereas inventory only holds a 10% to 25% collateral value. Your bank may require additional collateral if what is offered is less than the loan amount.

You can help your chances for approval by:

- Offering a larger amount of cash as a down payment.

- Offering personal assets if the business assets are not adequate.

- Ask EFund about a guaranteed loan product like an SBA 7a loan, which doesn’t have traditional collateral standards.

- Having a guarantor who is willing to pledge collateral for you.

5. Conditions

This is the C that you can control. It’s your explanation of general conditions that a lender relies on. You don’t have control of economic conditions or your competition. But you do have control of how you will act or react and can share this in your plan.

Your business plan or project summary plays a big role in conditions approval. Doing the planning and making a case for the lender to take a chance on you holds a lot of weight in the final lending decision.

One of the biggest reasons for loan turndowns is the lender doesn’t have the information they need to make a strong case.

6. Communication

As we mentioned earlier, we like to add a sixth C to the process – communication. Open communication with your EFund loan officer and/or advisor is key to your financial partnership.

When you face challenges, we want to know. We are here to help. When you have success, we want to know, too. We enjoy celebrating your successes with you. We will be with you for every step of the way.

If you have specific questions about applying for a business loan or the process, reach out to your advisor or contact us.

To learn more about business lending and when to consider applying for a loan, see our previous blog post.

.png)

.png)